Personal Finance Without Trust

I stopped giving my bank credentials to apps. Then I built the thing I actually wanted — a net worth tracker that lives on my device and never phones home.

TL;DR — I got paranoid about giving my bank credentials to finance apps. Instead of dealing with it like a normal person, I built my own net worth tracker. It reads PDF statements, lives on my device, and has never once phoned home. This is not a product launch. This is a coping mechanism.

I have twelve financial accounts. I know. It’s a lot.

Three bank accounts across two countries (career hopping does this to you). A brokerage. Two retirement funds. Some crypto I bought in 2021 during a moment of weakness that I now pretend doesn’t exist. A mortgage. A property. A small emergency fund in a different currency because apparently I enjoy making my own life harder.

That’s twelve accounts, four currencies, three institutions, and — until recently — absolutely no idea what I was actually worth. I had a rough feeling it was “probably fine” which, as it turns out, is not a number.

The standard advice is to sign up for an aggregator. Mint, YNAB, Copilot, Monarch, Empower — the personal finance app industrial complex has no shortage of options. Connect your banks, let them scrape your transactions every night, enjoy a pretty dashboard. Millions of people do this. I did this, for years.

Then I stopped. And now I’m that guy.

The trust problem

Here’s what actually happens when you click “Connect your bank” on one of those apps. Your credentials take a little road trip through at least three companies you’ve never met: the app itself, a data broker like Plaid or MX, and whoever their “analytics partners” are. (The quotes are doing heavy lifting there.) Your entire financial history ends up on servers you don’t control, governed by privacy policies that are designed to be long enough that you won’t read them.

Fun fact: Plaid settled a privacy lawsuit for $58 million in 2022 over allegations that they collected more data than users authorized and shared it beyond what was disclosed. I’m not saying they’re evil. I’m saying when the company whose entire job is “handle bank credentials responsibly” pays $58 million to make a lawsuit go away, maybe the trust chain deserves a second look.

Nobody stole my money. I didn’t have a breach scare. I just thought about it one afternoon — really thought about the architecture of who has access to what — and decided I didn’t love it. Call it paranoia. I call it reading the terms of service once, which was apparently once too many.

The problem was that the alternative — manually tracking twelve accounts in a spreadsheet — is a job I will never, ever, not in a million years do consistently. I know myself. That spreadsheet would be updated twice, very enthusiastically, and then abandoned forever. I needed something in between “give everyone your bank password” and “maintain a spreadsheet like a responsible adult.”

The gaps

These are not universal complaints. These are the specific things that annoyed me, personally, enough to spend weekends building something about it. Your list might be different. Your list might be “I don’t care, Mint is fine.” That’s valid. This is my neurosis.

Every app that shows one net worth number demands API access to all my accounts first. I just wanted assets minus liabilities. Basic arithmetic, held hostage by OAuth.

I hold assets in multiple currencies because I keep moving countries (see: career section). SGD 50,000 is worth different dollars every day. Most trackers either ignore this or get it hilariously wrong.

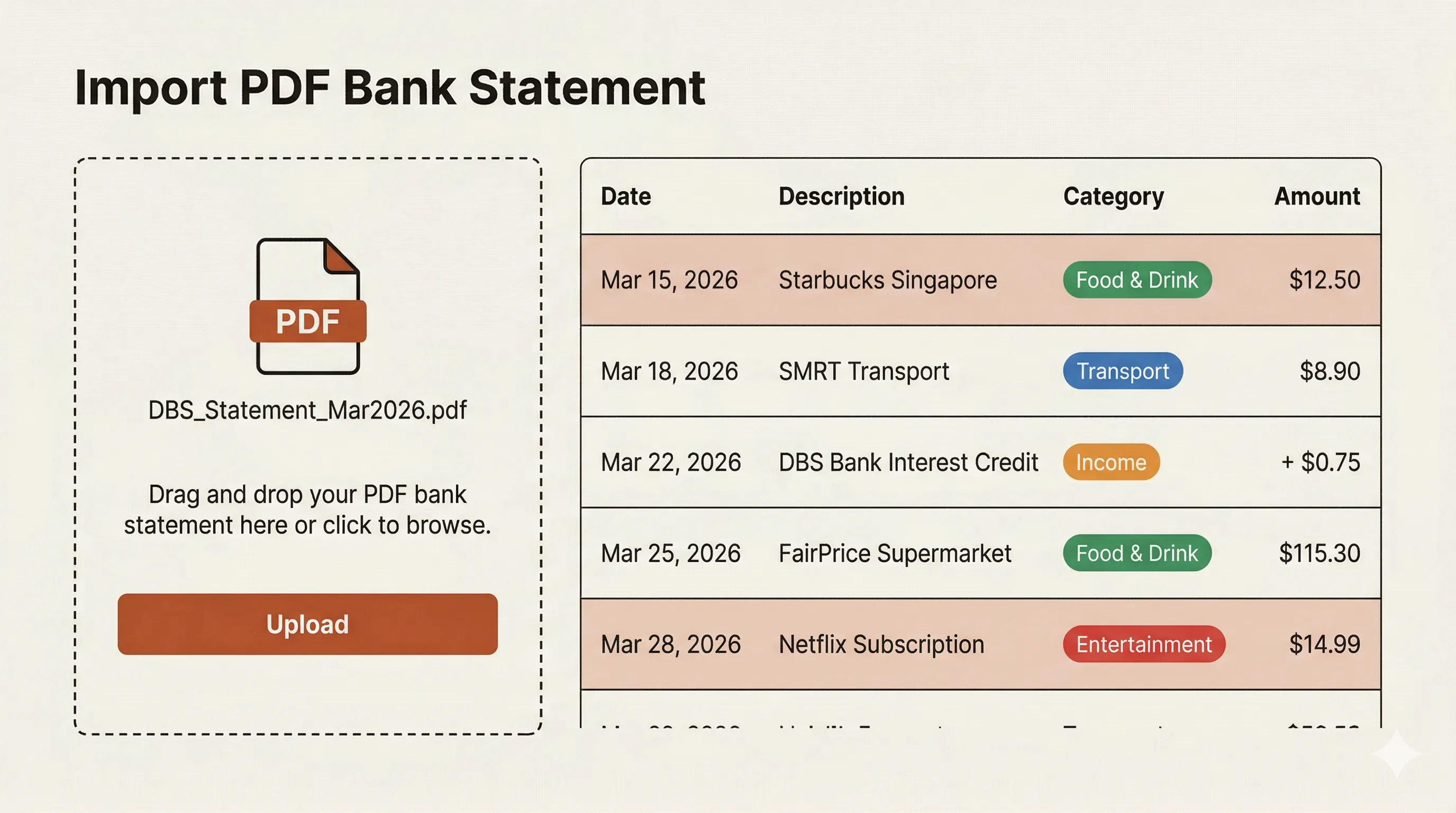

Every bank on earth emails me a PDF statement monthly. The one universal export format. And not a single app I tried could just… read it. They all want the API connection instead. The PDF sits there, full of data, ignored.

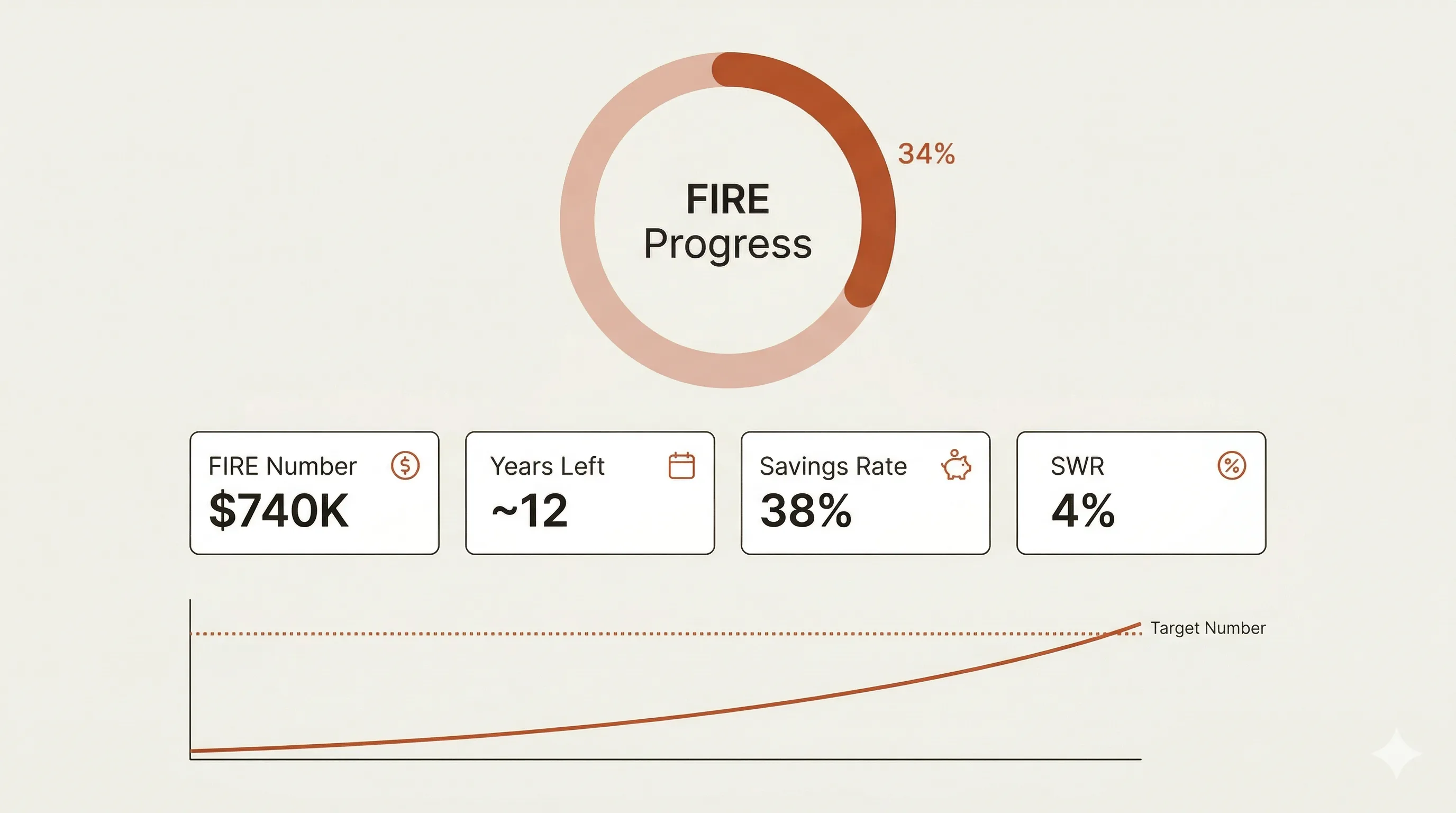

”When does working become optional?” — the only financial question that actually matters. No tool answered it without requiring me to become a spreadsheet person. I am not a spreadsheet person.

I wanted something that could look at my financial life and say “you don’t need that” before I buy another gadget I’ll use twice. Not a budget I’ll ignore — something with actual context.

Between moving countries and years of accumulating things, I genuinely stopped knowing what I own. Somewhere in a closet there’s probably a third charger for a device I no longer have.

What I built (because apparently that’s how I solve problems)

I built a web app I call Trezr. (Yes, I removed the vowels. It was 2024, we were all doing it. I’m not proud.)

It’s a net worth tracker built around one idea: your financial data stays on your device unless you decide otherwise. Not a product. Not a startup. Not a “what if we disrupted personal finance” pitch. Just a thing I built for myself because no existing tool scratched the exact itch I had, and I happen to be an engineer who responds to mild inconvenience by building software.

Here’s how it maps to each gap:

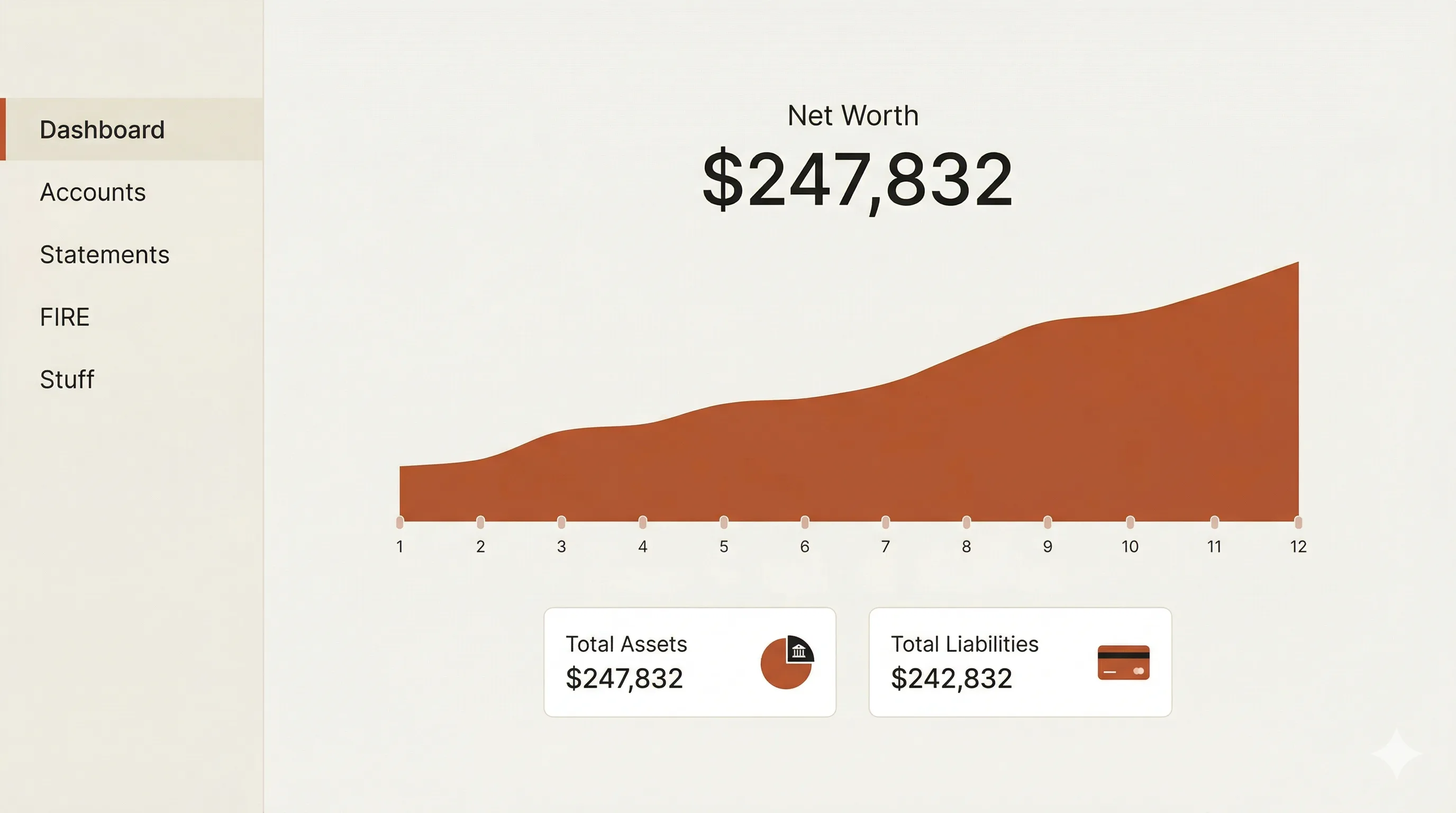

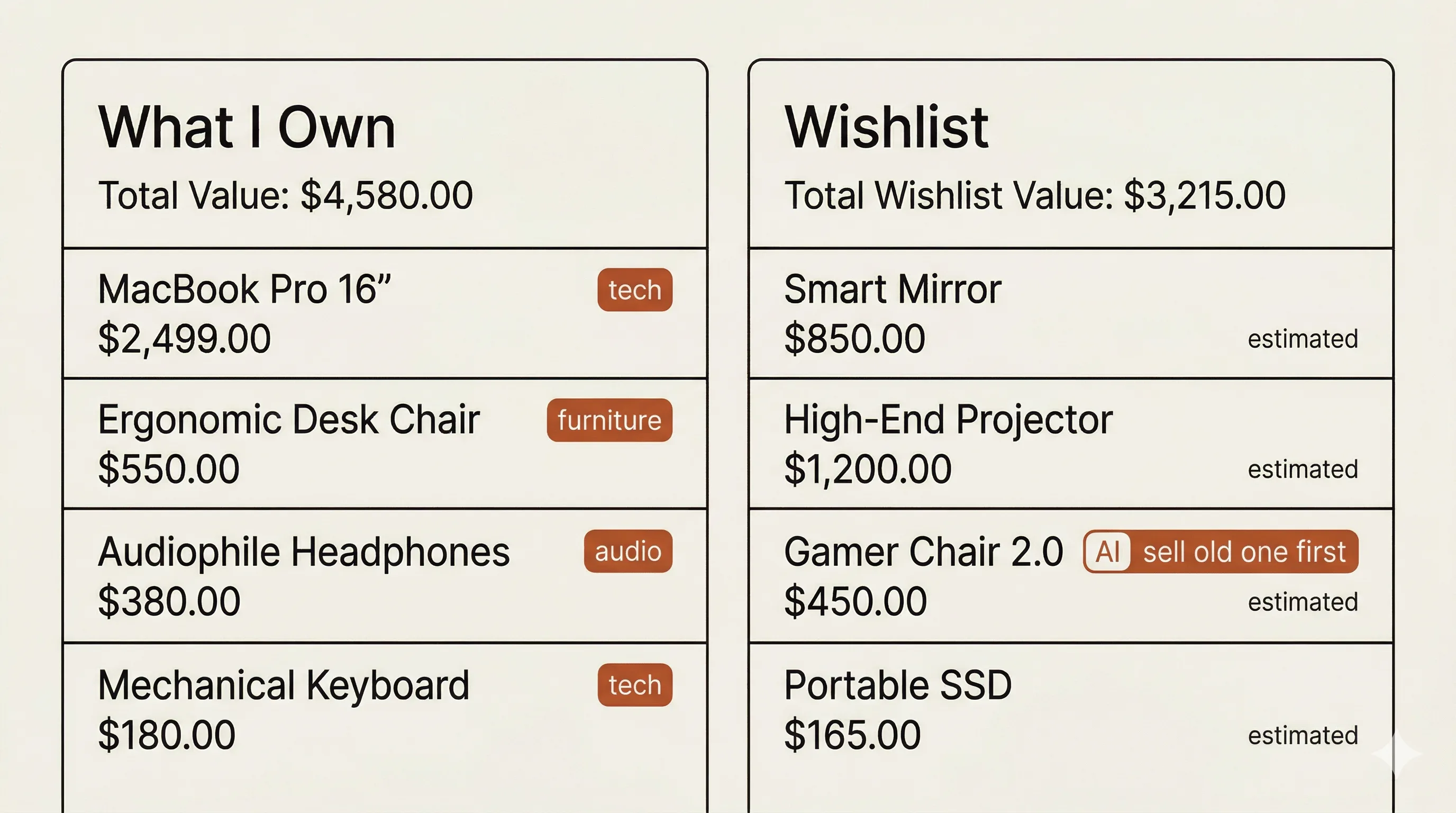

I add accounts by hand — balances, brokerage, crypto, property, debts. One number, one chart. Revolutionary technology: subtraction. I update monthly.

Every asset stays in its native currency. Real exchange rates, applied at snapshot time. The trend line is finally honest, which is more than I can say for most things in finance.

Upload a PDF, get transactions. Is it perfect? No, PDFs are a terrible format. Does it get the vast majority right? Yes. Good enough beats never-done-at-all.

FIRE number, progress bar, years remaining. All recalculated on reconcile. It’s a compass heading, not a prophecy. If the number goes down, good. If it goes up, time to panic. (Gently.)

Before I buy something dumb, I ask: “Should I buy this?” It knows my net worth, goals, and inventory. Sometimes: “no.” Sometimes: “yes, but sell the old one first.” My wallet’s therapist.

What I own, what I paid. An AI layer suggests what to sell or donate. The main revelation: I own significantly more things than I thought, and need approximately none of them.

Oh, and there are twelve net worth milestones from $1,000 to $10,000,000. When you hit one, confetti explodes on screen. Is it childish? Absolutely. Does it work? Also absolutely. Turns out the lizard brain doesn’t care that the confetti is fake.

What I gave up (honesty corner)

Let’s not pretend this is all upside. I gave up real things.

I don’t see yesterday’s transactions. My spending shows up in monthly chunks, which means if I want to know what I blew at the coffee shop this week, I have to open my banking app like some kind of caveman. I update stock prices and crypto manually — the app shows live market data, but my portfolio only updates when I tell it to. Setting the whole thing up took about twenty minutes, and reconciling takes fifteen minutes a month.

Fifteen minutes. That’s the price of not giving my bank credentials to a chain of companies I’ve never met. Honestly, I spend more time than that deciding what to watch on Netflix. The math works for me. Yours might not. That’s fine — I’m not your financial advisor, and if I were, you should probably get a new one.

The ritual

First week of the month. Fifteen minutes. Download PDFs from each bank. Upload them. Fix the three transactions the parser got wrong. Update asset values. Hit reconcile. Watch the chart move. Hope for confetti. Check the FIRE number. Close the tab. Go back to pretending I’m not thinking about money.

That’s it. A complete, private picture of my entire financial life. No credentials shared. No data on servers I don’t own. No anxiety about whether Plaid is having another bad year.

Why I wrote this

Not to convince you to build your own finance tracker. That would be unhinged advice for most people. “Just build your own app” is the software engineer equivalent of “have you tried not being sad?” — technically possible, deeply unhelpful.

I wrote this because the gap bugged me for years and I assumed it was unsolvable. Every tool wanted my bank credentials. The only alternative was spreadsheets, and I am fundamentally not a spreadsheet person. So I did nothing, and my financial picture stayed fragmented across twelve accounts and four currencies with no unified view and a vague sense that things were “probably fine.”

Building my own thing worked for me because I could. The actual point is that the gap exists. There’s a massive empty space between “hand over your bank password” and “be disciplined enough to maintain a spreadsheet” and almost nobody is filling it. The tradeoff between convenience and control is way more favorable than the aggregator companies want you to think.

Your bank statements are already on your device. They’re just sitting there. Full of data. Doing nothing.

I upload mine once a month. And the confetti — I’m not going to lie — the confetti keeps me coming back.